No, the Iran War Will Not Cement China’s Superpower Status

Response to The Financial Times

The Financial Times published an opinion piece today that I found genuinely thought-provoking, and worth engaging with given that I have argued, since the start of the operation, that its strategic consequences are weakening China.

The piece advances the claim that Operation Epic Fury ultimately advantages Beijing, arguing that China’s industrial prowess positions it to reap substantial economic and diplomatic gains from the conflict.

I want to walk through that argument carefully and explain why it falls short of establishing that the Iran war will cement China’s superpower status.

1- The Energy Question

Absorbing a shock and converting a crisis into a lasting strategic advantage are two very different propositions, and the distinction matters enormously here:

Before Operation Epic Fury, China enjoyed a tolerant and permissive sanctions environment in which Washington looked the other way as Beijing bought Iranian oil at discounts below market price.

That pricing advantage lowered the cost of Chinese production across every energy-intensive industry, giving Beijing's manufacturers a built-in edge over competitors who paid full market rates.

In fact, even the threat of U.S. sanctions turned out to not be useful: It was reported by the the Congressional Research Service in 2024 that “China's increasing imports of Iranian petroleum may demonstrate that PRC-based buyers believe that the economic benefits of buying Iranian petroleum exceed the risks of U.S. sanctions for several reasons.”

Washington had already begun closing that gap by tightening enforcement on Venezuelan oil, sanctioning the shadow tanker networks through which China imported roughly 389,000 barrels per day of Venezuelan crude at also steep discounts (roughly 4% of China’s total seaborne crude imports, according to Kpler data).

In this sense the Iran operation represents the same policy applied in a different theater. For China, replacing that supply through conventional channels means, once again, paying conventional prices.

“As part of Operation Southern Spear, the United States enacted a blockade on sanctioned oil tankers traveling in and out of Venezuela on 17 December 2025, after placing additional sanctions affecting oil trade with the country. A week before announcing the blockade, the US seized the oil tanker Skipperin the Caribbean Sea off the coast of Venezuela on 10 December, and then focused its military efforts on intercepting and pursuing other tankers trading with Venezuela.” Read More

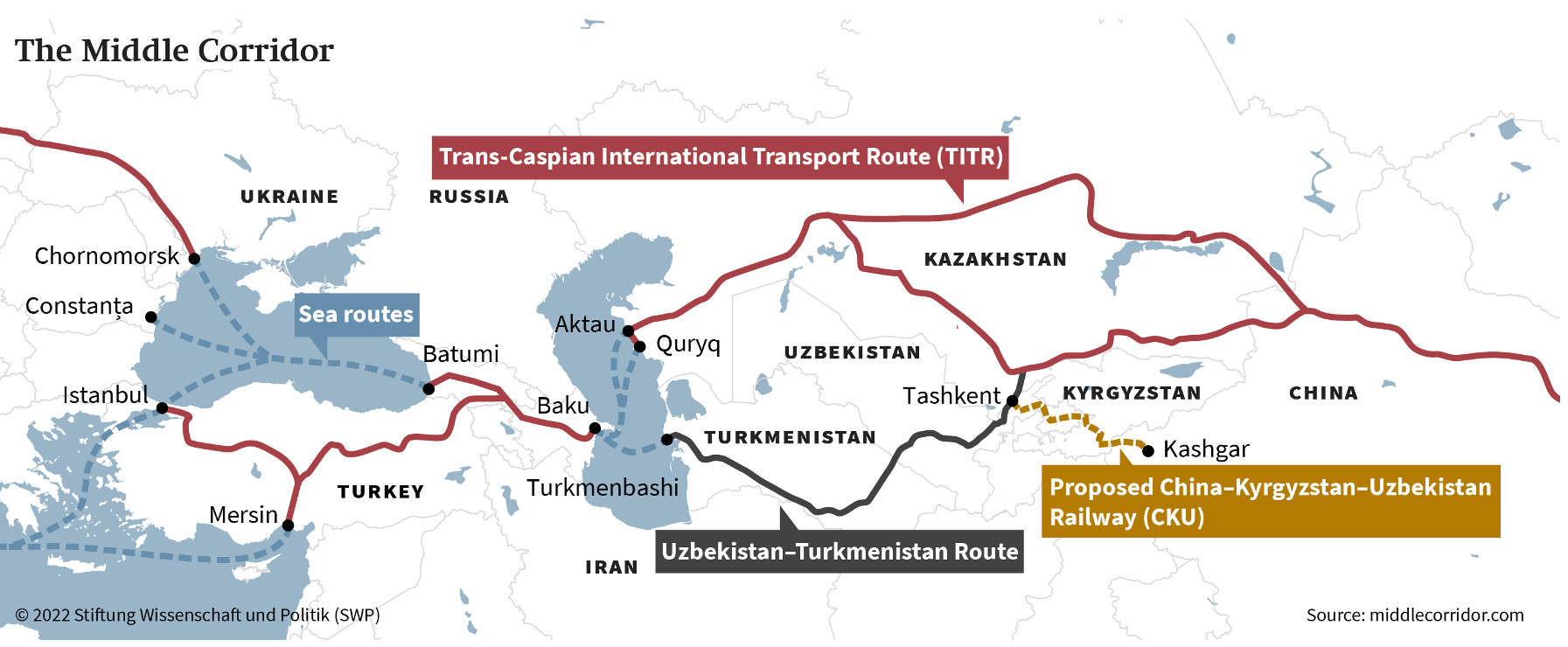

As for China’s contracts with Russia and Turkmenistan, they deserve some scrutiny:

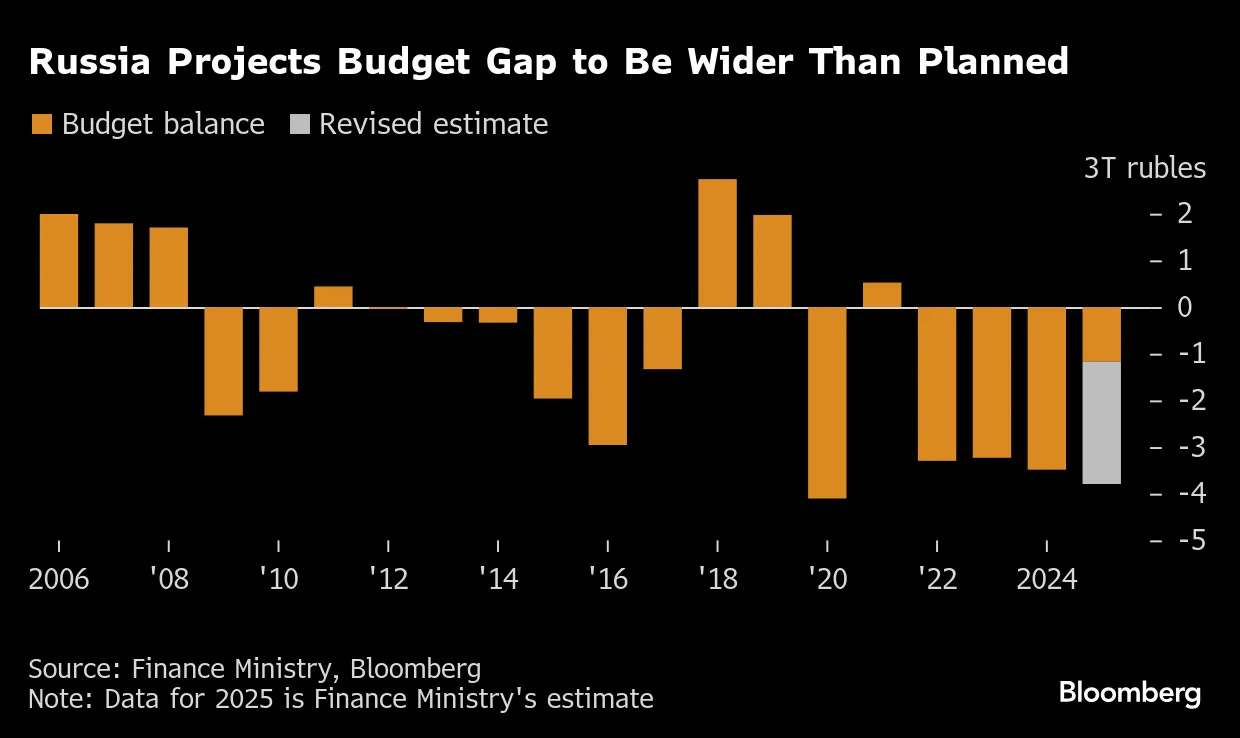

Russia recorded a budget deficit of 5.6 trillion roubles ($72.12 billion) equivalent to 2.6% of GDP in 2025 and with Moscow now attempting to sell $35 billion in seized assets simply to keep its budget functioning.

Beijing will grow increasingly dependent on a partner that is running out of money to honor its commitments. Russia's fiscal position is deteriorating under the combined weight of cascading sanctions and wartime spending, and that deterioration directly threatens its ability to maintain the infrastructure and export volumes that Chinese supply contracts depend on.

Regarding Turkmenistan in particular, the structural problem for Beijing is one of diminishing leverage over a supplier that is actively working to reduce its dependence on a single customer.

Turkmenistan holds the world's fourth largest gas reserves, and its leadership has made export diversification an explicit national priority, pursuing new pipeline routes toward Turkey and Europe precisely to escape the market concentration that has historically forced Ashgabat to accept unfavorable terms from Beijing.

China already pays a premium for Turkmen gas compared to what it pays for Russian supplies, and as Turkmenistan succeeds in attracting alternative buyers and building alternative routes, Beijing's ability to negotiate volume and price from a position of strength will erode further.

The supply from Turkmenistan will likely continue, but at progressively higher cost, which compounds rather than offsets the pricing pressure China is already absorbing from the loss of discounted Iranian and Venezuelan crude.

2- Cleantech and Other Commodities

Superpower status requires the ability to set the terms of both international and financial order, provide security guarantees other states rely on, and absorb economic shocks without rationing your own exports. China’s industrial capacity and usage of strategic reserves deliver none of those things.

China's dominance in electric vehicles, batteries, and solar panels reflects manufacturing scale and cost advantages. However that does not constitute geopolitical leverage because true leverage requires sustained dependency. The largest markets capable of generating such dependency are actively working to eliminate it.

Worth adding is that China's clean energy dominance was itself built on access to Western technology and export demand, the very channels now being systematically restricted, meaning the industrial base and the geopolitical returns it was supposed to generate are both under pressure simultaneously.

The United States, European Union, India, and Turkey (for antidumping duties on Chinese solar modules) have all raised tariff barriers against Chinese clean energy exports. China’s response has been to route production through third countries, but the EU is already tightening local content requirements that make third-country assembly insufficient to qualify for tariff exemptions, and the US has imposed anti-dumping duties on solar cells from Malaysia, Vietnam, Thailand, and Cambodia for doing exactly that.

“The U.S. Department of Commerce (Commerce) determines that, except as noted below, imports of certain crystalline silicon photovoltaic cells, whether or not assembled into modules (solar cells and modules), that have been completed in the Kingdom of Cambodia (Cambodia), Malaysia, the Kingdom of Thailand (Thailand), or the Socialist Republic of Vietnam (Vietnam), using parts and components produced in the People's Republic of China (China), as specified below, that are then subsequently exported from Cambodia, Malaysia, Thailand, or Vietnam to the United States are circumventing the antidumping duty (AD) and countervailing duty (CVD) orders on solar cells and modules from China.” Read More

In this case, the arbitrage window is closing faster than Beijing can exploit it. Also, stock market gains in Chinese battery companies following a geopolitical shock reflect investor sentiment, not a durable shift in competitive or geostrategic position, and the two shouldn’t be conflated.

Moreover, the claim that China can act as a supplier of last resort for fertilizer, sulphur, and helium does not hold up against the basic facts of each market.

On fertilizer, China has halted its own exports precisely because Operation Epic Fury has disrupted its domestic supply chains, meaning Beijing is managing a shortage at home while the argument requires it to be potentially solving one abroad.

On sulphur, China imported nearly 9.9 million tons in 2024 and depends on foreign sources for its supply despite strong domestic production. That makes Beijing a net importer of the very material being presented as a Chinese strategic asset, which is a straightforward factual problem with the claim.

On helium, Beijing has announced a domestic discovery and reported breakthroughs in purification technology, but announcing a discovery and producing commercially viable volumes at scale are separated by years of capital investment that haven’t yet happened and it’s not happening now which is the most important part.

In each case a real industrial development is being treated as a deployable geopolitical asset when the domestic conditions required to deploy it don’t yet exist.

3- Petroyuan, China, and Gulf Countries

The petroyuan argument is more fragile than it appears.

Iran settles its oil sales through a shadow banking system of front companies, small regional banks, and Dubai or Hong Kong-based entities using false invoices and fictitious transaction details, with roughly $9 billion flowing through this network in 2024 according FinCEN. That’s the financial infrastructure of a sanctioned state that is out of the dollar system, not a credible monetary alternative. It’s key to know the difference.

Moreover, the renminbi accounts for 8.5 percent of global foreign exchange, the US dollar, by contrast, remains overwhelmingly dominant, appearing on one side of 89.2% of all FX trades, and the yuan remains not yet fully convertible, meaning the petroyuan thesis requires Gulf states to anchor their fiscal systems to a currency they cannot freely trade on global markets, a proposition Riyadh has shown no serious appetite for. Saudi Arabia and the UAE together hold approximately $250 billion in US Treasuries, with GCC sovereign wealth funds managing more than $6 trillion overall, much of it dollar-denominated.

“Because the renminbi is not fully convertible for investment, it lacks the liquidity and accessibility required by international central banks. Central banks prefer safe, freely traded assets like the U.S. dollar, euro, Japanese yen, and British pound sterling.” Read More

It’s also important to highlight that Beijing brokered the 2023 Iran-Saudi normalization agreement and presented it as proof of its maturity as a reliable power, while simultaneously enabling Iran's access to export-controlled dual-use technology for its drone and missile programs through networks of transshipment companies. It was a level of involvement serious enough that 366 China and Hong Kong-based entities were placed on the US Specially Designated Nationals list for Iran-related sanctions programs.

Indeed, prior to Operation Epic Fury US special forces boarded a vessel in the Indian Ocean and removed components that were traveling from China to Iran to help IRGC rebuild its ballistic missile capabilities following the 12-day war.

In other words, the weapons architecture Beijing helped construct is the same one now implicated in Iranian strikes on Saudi territory. And Gulf capitals have drawn their own conclusions about what Chinese partnership delivers under pressure, and those conclusions are visible in where they are placing their security bets right now.

As a matter of fact, Riyadh is coordinating with Washington, not Beijing, on how to contain Iranian aggression. Similarly, the UAE, which signed the Abraham Accords and has spent the years since deepening its defense architecture with Washington, is consolidating its alignment.

Again, superpower status in practical terms means other states call you when the missiles start flying, denominate their reserves in your currency, and trust your diplomatic channels to hold when the pressure is on. On every one of those measures, the Gulf is turning to Washington, not Beijing.

Thank you for your work extrapolating the full reach and consequences of Epic Fury, and how the US policy has degraded China’s influence at so many levels.

Very enlightening.

Strong analysis on the petroyuan weakness and the clean energy tariff walls closing. You're right that manufacturing scale is not geopolitical leverage when your customers are actively building alternatives, and the Iran-Saudi brokering while arming Iran contradiction is something most China-optimists ignore.

But I think the framing is too binary. The question isn't whether this war "cements China's superpower status." China doesn't need superpower status to win from this war. It needs the US to be distracted, depleted, and discredited. All three are happening simultaneously.

A few points from my coverage:

China is the one country Iran is still letting through Hormuz. Chinese vessels are broadcasting "Chinese crew" status to secure passage through the IRGC's managed corridor. China is buying oil while everyone else is rationing. That's not replacing the dollar order. It's exploiting the collapse of the current one in real time.

China controls 80% of global tungsten production and imposed export controls in 2025. The US cannot replenish its munition stockpiles without Chinese supply chains. RUSI estimates 11,000 munitions expended in 16 days at $26 billion. Tomahawk production is 90 per year. The US has fired 850. The industrial base that needs to replenish these stocks runs through China. Beijing doesn't need to fire a shot. It just needs to not sell tungsten.

The diplomatic track is also shifting. Pakistan hosted Saudi Arabia, Turkey, and Egypt in Islamabad last week to mediate. Not Washington. Not Beijing. But the mediators are moving away from the US orbit, not toward it. China doesn't need to mediate. It needs everyone else to stop relying on the US for security guarantees, and that's exactly what's happening as Gulf state basing nations watch their refineries burn.

Your definition of superpower requires "setting the terms of international order, providing security guarantees, absorbing shocks without rationing." By that standard, the US isn't a superpower right now either. It can't guarantee Gulf state security (13 bases rendered uninhabitable). It can't absorb the oil shock ($116 and climbing toward $200). It can't set the terms of Hormuz (Iran sets them, at $2M per vessel).

The system is fragmenting. China benefits from fragmentation without needing to replace the US at the center. That's the more dangerous outcome than "superpower status," and it's already underway.

I've covered the Hormuz mechanics, the munitions math, and the coalition fracture in detail: https://tatsuikeda.substack.com/p/the-sovereign-chokepoint-how-iran